Brokerage Reports, Advisory Services and Investment Advisors

by

Charles Lamson

Brokerage Reports

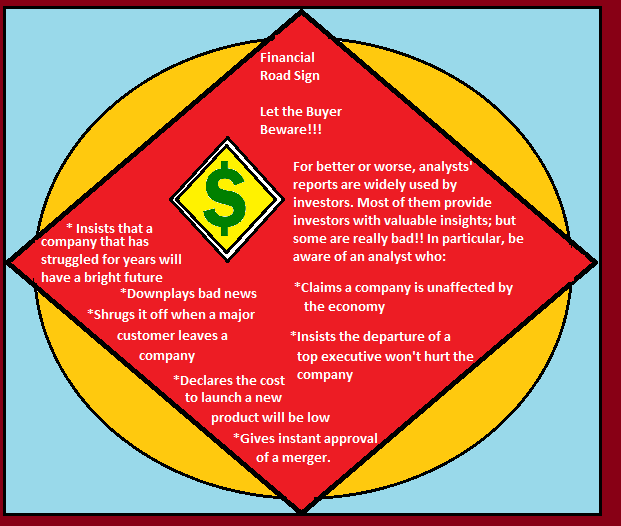

The reports produced by the research staffs of the major (full service) brokerage firms provide yet another important source of investor information. These reports cover a wide variety of topics, from economic and market analyses to industry and company reports, news of special situations, and reports on interest rates and the bond market. Reports on certain industries or securities prepared by the house's backoffice research staff may be issued on a regular basis and contains lists of securities within certain industries classified as to the type of market behavior they are expected to exhibit. Brokerage houses also regularly issue reports, prepared by their security analysts, on specific securities, which include among other things their recommendations as to the type of investment returns expected, and whether to buy, hold, or sell the securities in question.

Advisory Services

A number of subscription advisory services---available both in print and online---provide information and recommendations on various industries and specific securities. The services normally cost from $50 to several hundred dollars a year. Although these costs may be tax deductible, only the most active investors will find them worthwhile, because you can usually review such materials (for free) at your broker's office, at universities and public libraries, or online. Probably the best known financial services are those provided by Standard & Poor's, Moody's Investor Service, and Value Line Investment Survey. Each offers an array of services. Standard & Poor's publishes a monthly stock guide and bond guide, each of which summarizes the financial conditions of a few thousand issues. Moody's also publishes stock and bond guides. And a number of reports are also prepared weekly, like Standard & Poor's Outlook.

Recommended lists of securities, broken down into groups on the basis of investment objectives, constitute still another type of service. In addition to the popular subscription services, numerous investment letters, which periodically advise advisors on the purchase and sale of securities, are available. Finally, by subscribing to weekly chart books, investors may also obtain graphs showing stock prices and volume over extended periods of time.

Investment Advisors

Successful investors often establish themselves as professional investment advisors. In this capacity they attempt to develop investment plans consistent with the financial objectives of their clients. You can obtain the services of a professional money manager in several ways: (1) you can hire an independent investment advisor (but they're usually pretty expensive and prefer to deal with well-healed clients); (2) you can go to the trust department of a major bank (many offer their investment services to the general public at very reasonable costs, and you do not have to die or have a trust account to obtain such services---all you have to do is enter into a simple agency agreement ); (3) if you deal with a full-service brokerage firm, you can check with your broker to see if they offer fee-based wrap accounts (in these portfolio management accounts, your brokerage firm takes over the full-time management of your investments, in return for a flat annual fee---but watch out, that annual fee can get pretty hefty); or (4) you might consider the services of a financial planner (preferably a fee-based planner who has a strong track record in the field of investments).

If you are thinking of using a professional money manager, the best thing to do is shop around---look at the kinds of returns he or she has been able to generate (in good markets and bad), and do not overlook the matter of cost---find out up front how much you will have to pay and what the fee is based on. Annual fees for advisory services, which may involve the complete management of the client's money, are likely to range from about 1 percent to as much as 2 or 3 percent of assets under management. Equally important, find out if the advisor has a specialty and, if so, make sure it is compatible with your investment objectives.

*SOURCE: PERSONAL FINANCIAL PLANNING, 10TH ED., 2005, LAWRENCE J. GITMAN, MICHAEL D. JOEHNK, PGS. 465-467*

end

|

No comments:

Post a Comment