It is legal because I wish it.

Real Estate Mortgages (part A)

by

Charles Lamson

A mortgage is an interest in real estate given to secure the secure the payment of a debt. The mortgage does not constitute the debt itself but the security for the debt. If the debt is not paid the property may be sold to pay the debt. Land or any interest in land may be mortgaged. Land maybe mortgage separately from the improvements, or the improvements may be mortgaged apart from the land. A person who gives a mortgage as a security for a debt is a mortgagor. A person who holds a mortgage as property for a debt is a mortgagee.

|

The mortgagor normally retains possession of the property. In order for the mortgagee to obtain the benefit of the security, the mortgagee must take possession of the premises upon default or sell the mortgaged property at a foreclosure sale. In some states, the mortgagee may not take possession of the property upon default but may obtain the appointment of a receiver to collect the rents and income. If the sale of the property brings more than the debt and the costs, the mortgagor must be paid the balance.

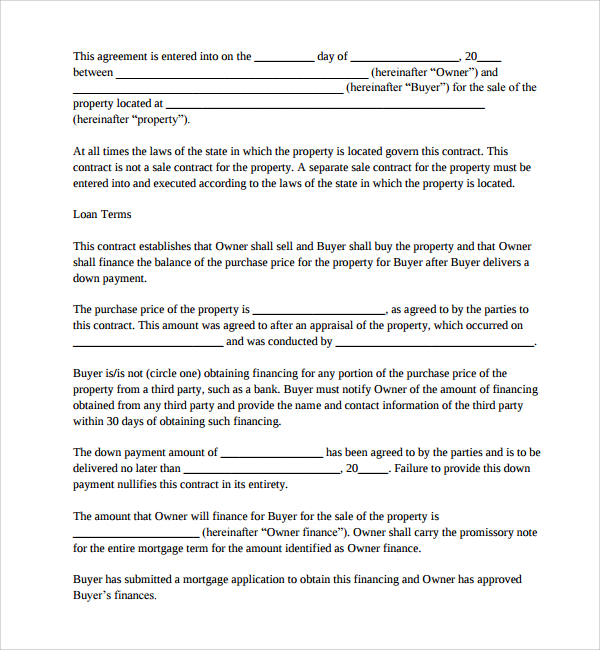

The Mortgage Contract

A mortgage must be in writing. The contract, as a rule, must have the same form as a deed, which means it must be acknowledged. The mortgage, like all other contracts sets forth the right and the duties of the contracting parties (see Illustration 1). As a type of contract, mortgages are interpreted according to contract law rules.

ILLUSTRATION 1 Mortgage Contract

A mortgagor normally gives a mortgage to raise money for the purchase price of real estate, but it may be given for other reasons. One may borrow money for any reason and secure the loan by a mortgage. One may assume a contingent liability for another, such as becoming a surety, and receive a mortgage as security.

The effect of a mortgage is to be a lien against the mortgaged property. A lien is an encumbrance or claim against property. The lean of the mortgage attaches to the property described in the mortgage. A mortgage generally also provides that the lien attaches to additions thereafter made to the described property; for example, the lien of the mortgage attaches to personal property, which thereafter becomes a fixture. A clause purporting to make the security clause of a mortgage becomes a fixture. A clause purporting to make the security clause of a mortgage cover future debts will be valid if the parties intended it to cover future debts.

Recording

Depending upon the law of the state in which the land lies, the mortgage gives the mortgagee either a lien on the land or title to the land. The mortgagor's payment of the debt divests or destroys this title or lien. Recording the mortgage protects the mortgagee against subsequent creditors, since the public record normally constitutes notice to the whole world as to the mortgagee's rights. There may be both a first mortgage and subsequent, or junior, mortgages. The mortgage recorded first normally has preference. This is not true of when actual notice of a prior mortgage exists. However, a purchase money mortgage has preference over other claims arising through the mortgagor. The mortgage is also recorded to notify its subsequent purchasers that as much of the purchase price as is necessary to pay off the mortgage must be paid to for the mortgagee. Recording must be proper, otherwise the purpose of the mortgagee providing notice to others cannot be accomplished.

Duties of the Mortgagor

The mortgagor assumes three definite duties and liabilities when placing a mortgage upon real estate. These pertain to:

Interest and Principal

The mortgagor must make all payments of interest and principal as they become due. Most mortgages call for periodic payments, such as monthly, semiannually, or annually. These payments are used to pay all accrued interest to the date of payment, and the mortgagee applies the balance on the principal. Other mortgages call for periodic payment of interest and for the payment of the entire principal at one time. In either case, a failure to pay either the periodic payments of interest and principal or of interest only constitutes a default. A default gives the mortgagee the right to foreclose. Most mortgages contain a provision that if the mortgagor does not make an interest or principal payment when due or within a specified time after due, the mortgagee may declare the entire principal immediately due. This is known as an acceleration clause.

If the mortgagor wishes to pay off the mortgage debt before the due date so as to save interest, that right must be reserved at the time the mortgage is given.

Taxes, Assessments, and Insurance Premiums

The mortgagor, who is the owner of the land regardless of the form of the mortgage, must continue to make such payments as would be expected of an owner of land. The mortgagor must pay taxes and assessments. If the mortgagor has not paid the taxes and assessments, the mortgagee must pay them and compel a reimbursement from the mortgagor. If the mortgage contract requires the mortgagor to pay these charges, a failure to pay them becomes a default.

The law does not require the mortgagor to keep the property insured nor to insure it for the benefit of the mortgagee. This duty cannot be imposed on the mortgagor by the mortgage contract. Both the mortgagor and mortgagee have an insurable interest in the property to the extent of each one's interest or maximum loss.

Security of the Mortgagee

The mortgagor must do not act that will materially impair the security of the mortgagee. Cutting timber, tearing down buildings, and all acts that waste the assets impair the security and give the mortgagee the right to seek legal protection. Some state statutes provide that any one of these acts constitutes a default. This gives the mortgagee the right to foreclose. Other statues provide only that the mortgagee may obtain an injunction in a court of equity enjoining any further impairment. Some states provide that for the appointment of a receiver to prevent waste. Many state laws also make it a criminal offence to willfully impair the security of mortgaged property.

*SOURCE: BUSINESS FOR LAW, 15TH ED., 2005, JANET E. ASHCROFT. J.D., PGS. 516-520*

end

|

No comments:

Post a Comment