The Money Supply and the Federal Reserve

(Part D)

by

Charles Lamson

|

The Modern Banking System

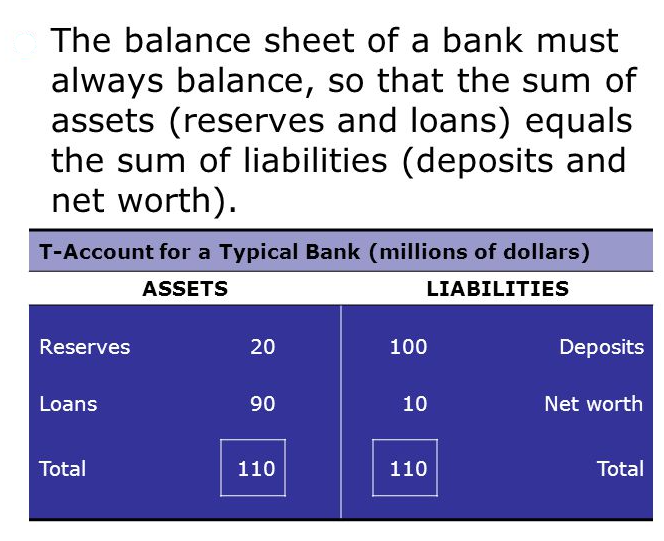

To understand how the modern banking system works, you need to be familiar with some basic principles of accounting. Once you are comfortable with the way banks keeps their books, the whole process of money creation will seem logical. A brief review of accounting Central to accounting practices is the statement that "the books always balance." In practice, this means that if we take a snapshot of a firm---any firm, including a bank---at a particular moment In time, then by definition: Assets - Liabilities ≡ Net Worth, or Assets ≡ Liabilities + Net Worth Assets are things a firm owns that are worth something. For a bank, these assets include the bank building, its furniture, its holdings of government securities, cash in its vault, bonds, stocks, and so forth. Most important among the bank's assets, for our purposes at least, are its loans. A barrower gives the bank an IOU, a promise to repay a certain sum of money on or by a certain date This promise is an asset to the bank because it is worth something. The bank could (and sometimes does) sell the IOU to another bank for cash. Other bank assets include cash on hand (sometimes called vault cash) and deposits with the United States' central bank the Federal Reserve Bank (the Fed). Federal banking regulations require that banks keep a certain portion of their deposits on hand as vault cash or on deposit with the Fed.  A firm's liabilities are its debts---what it owes. A bank's liabilities are the promises to pay, or IOUs, that it has issued. A bank's most important liabilities are its deposits. Deposits are debts owed to the depositors, because when you deposit money in your account, you are in essence making a loan to the bank. The basic rule of accounting says that if we add up a firm's assets and then subtract the total amount it owes to all those who have lent it funds, the difference is the firm's net worth. Net worth represents the value of the firm to its stockholders or owners. How much would you pay for a firm that owns $200,000 of diamonds and had borrowed $150,000 from a bank to pay for them? The firm is worth $50,000---the difference between what it owns and what it owes. If the price of diamonds were to fall, bringing their value down to only $150,000, the firm would be worth nothing. We can keep track of a bank's financial position using a simplified balance sheet called a T-account. By convention, the bank's assets are listed on the left side of the T-account and its liabilities and net worth, on the right side. By definition, the balance sheet always balances, so that the sum of the items on the left side of the T-account is exactly equal to the sum of the items on the right side. The T-account in Figure 1 shows a bank having $110 million in assets, of which $20 million dollars are reserves, the deposits that the bank has made at the Fed and its cash on hand (coins and currency). Reserves are an asset to the bank because it can go to the Fed and get cash for them, just the way you can go to the bank and get cash for the amount in your savings account. Our bank's other asset is its loans, worth $90 million. FIGURE 1  Why do banks hold reserves/deposits at the Fed? There are many reasons, but perhaps the most important is the legal requirement that they hold a certain percentage of their deposit liabilities as reserves. The percentage of its deposits that a bank must keep as reserves is known as the required reserve ratio. If the reserve ratio is 20 percent, Then a bank with deposits of $100 million must hold $20 million as reserves, either as cash or as deposits at the Fed. To simplify, we will assume that banks hold all of their reserves in the form of deposits at the Fed.  On the liability side of the T-account, the bank has taken deposits of $100 million, so it owes this amount to its depositors. This means that the bank has a net worth of $10 million to its owners ($110 million in assets - $100 million in liabilities = 10 million dollars net worth). The net worth of the bank is what "balances" the balance sheet. Remember: If a bank's reserves increase by $1 then one of the following must also be true: (1) its other assets (e.g., loans) decrease by $1; (2) its liabilities (deposits) increase by $1; or (3) its net worth increases by $1. Various fractional combinations of these are also possible.  *CASE & FAIR, 2004, PRINCIPLES OF ECONOMICS, 7TH ED., PP. 481-482* end |

No comments:

Post a Comment