TOP STORIES

Search Results

Endangered pallid sturgeon caught along Missouri River near Parkville

Kansas City Star-5 hours ago

Winders leads an effort in Missouri to bring the fish back. At one point, when theMissouri River was wild and unharnessed, pallid sturgeon ...

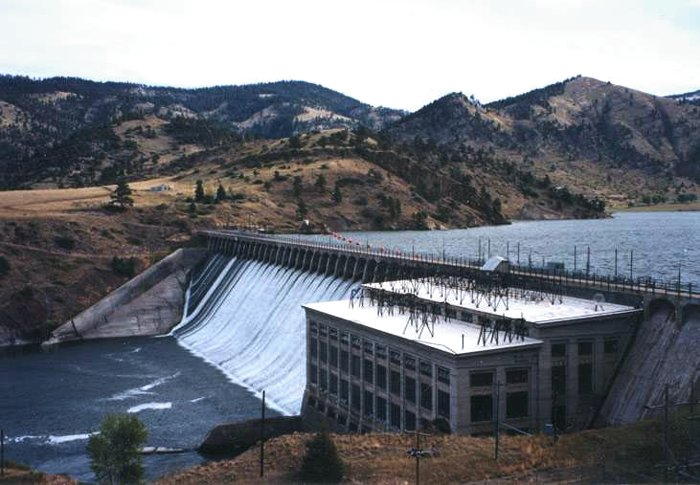

Montana's greatest wonder: Missouri River

Sidney Herald Leader-8 hours ago

When the Missouri River puts Cascade behind, it looks out toward the sunset and the distant Rocky Mountain Front, the range of mountains that ...

Man found dead in Missouri River

Daily Republic-8 hours ago

Man found dead in Missouri River. By Daily ... A 73-year-old man from Kimball was found dead in the Missouri River on Monday afternoon.

The Cost of Home Ownership

by

Charles Lamson

Although there definitely are some strong emotional and financial reasons for owning a home, there is still the question of whether you can afford to own one. There are two important aspects to the consideration of affordability: You must produce the down payment and other closing costs, and also be able to meet the cash-flow requirements associated with monthly mortgage payments and other home maintenance expenses. In particular, there are five items you should consider when evaluating the cost of home ownership to determine how much you can afford: the down payment, points and closing costs, mortgage payments, property taxes and insurance, and maintenance and operating expenses.

| ||

The Down Payment

The first major hurdle is the down payment. Most buyers finance a major part of the purchase price of the home, but they are required by lenders to invest money of their own, called equity. The actual amount of down payment required varies among lenders, mortgage types, and properties. To determine the amount of down payment that will be required in specific instances, lenders use the loan-to-value ratio, which specifies the maximum percentage of the value of a property that the lender is willing to loan. For example, if the loan-to-value ratio is 80 percent, the buyer will have to come up with a down payment equal to the remaining 20 percent.

Generally, first-time homebuyers must spending a number of years accumulating enough money to afford the down payment and other costs associated with a home purchase. You can best accumulate these funds if you plan ahead, using future value techniques to determine the monthly or annual savings necessary to have a stated amount by a specific future date. A disciplined savings program is the best way to obtain the funds needed to purchase a home or any other big-ticket item requiring a sizable down payment or cash outlay.

If you do not have enough savings to cover the down payment and closing costs, you can consider several other sources. You may be able to obtain some funds by withdrawing (subject to legal limitations) your contributions from your company's profit sharing or thrift plan. Your IRA is another option. The Taxpayer Relief Act of 1997 permits first-time homebuyers to withdraw $10,000 without penalty before age 59.5. However, using retirement money should be a last resort because you must still pay income tax on retirement distributions. Thus, if you are in the 25 percent income tax bracket, your $10,000 IRA withdrawal would net you only $7,500 ($10,000 - $2,500) for your down payment.

The Federal National Mortgage Association (known as "Fannie Mae") has several programs to help buyers who have limited cash for the down payment and closing costs. The "Fannie 3/2" program is available from local lenders. Borrowers who meet certain income criteria may qualify for a 95 percent loan-to-value mortgage, and may obtain up to 2 percent of their 5 percent down payment from a public or nonprofit agency or relative. "Fannie 97" helps the homebuyer who can handle monthly mortgage payments but does not have cash for the down payment. It requires only a 3 percent down payment from the borrower's own funds, and the borrower needs to have only 1 month's mortgage payment in cash savings, or reserves, after closing.

As a rule, when the down payment is less than 20 percent, the lender will require the buyer to obtain private mortgage insurance (PMI), which protects the lender from loss if the borrower defaults on the loan. Usually, PMI covers the lender's risk above 80 percent of the price of the house. Thus, with a 10 percent down payment, the mortgage will be a 90 percent loan, and mortgage insurance will cover 10 percent of the home's price. The cost of mortgage insurance varies from about 0.5 percent to 1.0 percent of the loan balance each year, depending on the size of your down payment. It can be included in your monthly payment, and the average cost ranges from about $40 to $70 per month. You should contact your lender to cancel the mortgage insurance once the equity in your home reaches 20 to 25 percent. Under federal law, private mortgage insurance on most loans made on or after July 29, 1999, end automatically once the mortgage is paid down to 78 percent of the original value of the house.

Points and Closing Costs

A second hurdle to home ownership relates to mortgage points and closing costs. Mortgage points are fees charged by lenders at the time they grant a mortgage loan. In appearance, points are like interest in that they are a charge for borrowing money. They are related to the lender's supply of loanable funds and the demand for mortgages; the greater the demand relative to the supply, the more points you can expect to pay. One point equals 1 percent of the amount borrowed. If you borrow $100,000 and loan fees equal 3 points, the amount of money you will pay in points will be $100,000 x .03 = $3,000.

Lenders typically use points as a way of charging interest on their loans. They can vary the interest rate along with the number of points they charge to create loans with comparable effective rates. For example, a lender might be willing to give you a 7 percent rather than an 8 percent mortgage if you are willing to pay more points; that is, you choose between an 8 percent mortgage rate with 1 point or a 7 percent mortgage rate with 3 points. If you choose the 7 percent loan, you will end up paying a lot more at closing (although the amount of interest paid over the life of the mortgage may be considerably less).

Points increase the effective rate of interest on a mortgage. The amount you pay in points and the length of time you hold a mortgage determine the increase in the effective interest rate. For example, on an 8 percent, 30-year, fixed-rate mortgage, each point increases the annual percentage rate by about .11 percent if the loan is held for 30 years, .17 percent if held for 15 years, .32 percent if held 7 years, and .70 percent if held 3 years. you pay the same amount in points regardless of how long you keep your home. Therefore, the longer you hold the mortgage, the longer the period over which you amortize the points and the smaller the effect of the points on the effective annual interest rate.

According to recent IRS rulings, the points paid on a mortgage at the time a home is originally purchased are usually considered immediately tax deductible. The same points are not considered immediately tax deductible if they are incurred when refinancing a mortgage; rather, the amount paid in points must be written off (amortized) over the life of the new mortgage loans.

Closing costs are all expenses that borrowers ordinarily pay at the time a mortgage loan is closed and title to the purchased property is conveyed to them. Closing costs are like down payments. They represent money you must come up with at the time you buy the house. Closing costs are made up of such items as loan application and loan organization fees paid to the lender, mortgage points, title search and insurance fees, attorney's fees, appraisal fees, and other miscellaneous fees for things such as mortgage taxes, filing fees, inspections, credit reports, and so on. These costs can amount to 50 percent or more of the down payment. For example, with a 10 percent down payment on a $100,000 home, the closing costs are nearly 70 percent of the down payment, or $6,625. Simple arithmetic indicates that this buyer will need nearly $17,000 to buy the house (the $10,000 down payment plus another $6,625 in closing costs).

*SOURCE: PERSONAL FINANCIAL PLANNING, 10TH ED., 2005, LAWRENCE J. GITMAN, MICHAEL ED. JOEHNK, PGS. 194-196*

end

|

No comments:

Post a Comment