Common and Preferred Stock Financing

(Part D)

by

Charles Lamson

Provisions Associated with Preferred Stock

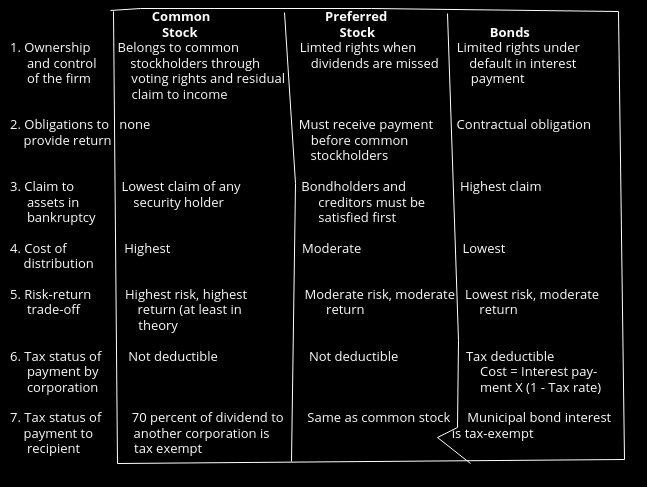

A preferred stock issue contains a number of stipulations and provisions that define the stockholder's claims to income and assets. 1. Cumulative Dividends Most issues are cumulative preferred stock and have a cumulative claim to dividends. That is, if preferred stock dividends are not paid in any one year, they accumulate and must be paid in total before common stockholders can receive dividends. If preferred stock carries a $10 cash dividend and the company does not pay dividends for 3 years, preferred stockholders must receive the full $30 before common stockholders can receive anything. The cumulative dividend feature makes a corporation very aware of its obligation to preferred stockholders. When a financially troubled corporation has missed a number of dividend payments under a cumulative arrangement, there may be a financial recapitalization of the corporation in which preferred stockholders receive new securities in place of the dividend that is in arrears (unpaid). Assume the corporation has now missed five years of dividends under a $10 a year obligation and the company still remains and a poor cash position. Preferred stockholders may be offered $50 or more in new common stock or bonds as forgiveness of the missed dividend payments. Preferred stockholders may be willing to cooperate in order to receive some potential benefit for the future. 2. Conversion Feature Like certain forms of debt, preferred stock may be convertible into common shares. Thus, $100 in preferred stock may be convertible into a specified number of shares of common stock at the option of the holder. One wrinkle on convertible preferreds is the use of convertible exchangeable preferreds that allow the company to force conversion from convertible preferred stock into convertible debt. This can be used to allow the company to take advantage of falling interest rates or to allow the company to change preferred dividends and to tax deductible interest payments when it is to the company's advantage to do so. This topic of convertibility will be discussed at length in future posts covering convertibles, warrants, and derivatives.  3. Call Feature Also, preferred stock, like debt, may be callable; that is, a corporation may retire the security before maturity at some small premium over par. This, of course, accrues to the advantage of the corporation and to the disadvantage of the preferred stockholder. A preferred issue carrying a call provision will be accorded a slightly higher yield than a similar issue without this feature. This same type of refunding decision applied to debt obligations could also be applied to preferred stock. 4. Participation Provision A small percentage of preferred stock issues are participating preferreds; that is, they may participate over and above the quoted yield when the corporation is enjoying a particularly good year. Once the common stock dividend equals the preferred stock dividend, the two classes of securities may share equally in additional payouts. 5. Floating Rate Beginning in the 1980s, a few preferred stock issuers made the dividend adjustable in nature and the stock is classified as floating rate preferred stock. Typically the dividend is changed on a quarterly basis, based on current market conditions. Because the dividend rate only changes quarterly, there is still some possibility of a small price change between dividend and adjustment date. Nevertheless, it is less than the price change for regular preferred stock. Investors that participate in floating rate preferred stock do so for two reasons: to minimize the risk of price changes and to take advantage of the tax benefits associated with preferred stock corporate ownership. The price stability actually makes floating rate preferred stock the equivalent of a safe short-term investment even though preferred stock is normally thought of as long-term in nature.  6. Dutch Auction Preferred Stock Dutch auction preferred stock is similar to floating-rate preferred stock but is a short-term instrument. The security matures every seven weeks and is sold (reauctioned) at a subsequent bidding. The concept of Dutch auction means the stock is issued to the bidder willing to accept the lowest yield and then to the next lowest bidder and so on until all the preferred stock is sold. This is much like the treasury bill auctions held by the Federal Reserve Bank. This auction process at short-term intervals allows investors to keep up with the changing interest rates in the short-term market. Some corporate investors like Dutch auction preferred stock because it allows them to invest at short-term rates and take advantage of the tax benefits available to them with preferred stock Investments. 7. Par Value A final important feature associated with preferred stock is par value. Unlike the par value of common stock, which is often only a small percentage of the actual value, the par value of preferred stock is set at the anticipated market value at the time of issue. The par value establishes the amount due to preferred stockholders in the event of liquidation. Also, the par value of preferred stock determines the base against which the percentage or dollar return on preferred stock is computed. Thus, 10 percent preferred stock would indicate $10 a year in preferred dividends if the par value were $100, but only $5 annually if the par value were $50. Comparing Features of Common and Preferred Stock and Debt In Table 3, we compare the characteristics of common stock, preferred stock, and bonds. The student should consider the comparative advantages and disadvantages of each. Table 3 Features of alternative security issues  In terms of the risk-return features of these three classes of securities and also of other investments, we might expect the risk-return patterns depicted in Figure 1. The lowest return is obtained from savings accounts, and the highest return and risk are generally associated with common stock. In between, we note that short-term instruments generally, though not always, provide lower returns than longer-term instruments. We also observe that government securities pay lower returns than issues originated by corporations, because of the lower risk involved. Next on the scale after government issues is preferred stock. This hybrid form of security generally pays a lower return than even well-secured corporate debt instruments, because of the 70 percent tax exempt status of preferred stock dividends to corporate purchasers. Thus the focus on preferred stock is not just on risk-return trade-off but also on after tax return. Figure 1 Risk and expected return for various security classes   Next, we observe increasingly high return requirements on debt, based on the presence or absence of security provisions and the priority of claims on unsecured debt. At the top of the scale is common stock. Because of its lowest priority of claim in the corporation and its volatile price movement, it has the highest demanded return. Though extensive research has tended to validate these general patterns, short-term or even intermediate-term reversals have occurred, in which investments with lower risk have outperformed investments at the higher end of the risk scale. Summary Common stock ownership carries three primary rights or privileges. There is a residual claim to income. All funds not paid out to other classes of securities automatically belong to the common stockholder; the firm may then choose to pay out these residual funds in dividends or to reinvest them for the benefit of common stockholders. Because common stockholders are the ultimate owners of the firm, they alone have the privilege of voting. To expand the role of minority stockholders, many corporations use a system of cumulative voting, in which each stockholder has voting power equal to the number of shares owned times the number of directors to be elected. Buy cumulating votes for a small number of selected directors, many stockholders are able to have representation on the board.  Common stockholders may also enjoy a first option to purchase new shares. This privilege is extended through the procedure known as a rights offering. A shareholder receives one right for each share of stock owned and may combine a certain number of rights, plus cash, to purchase a new share. While the cash or subscription price is usually somewhat below the current market price, the stockholder neither gains nor loses through the process. A poison pill represents a rights offer made to existing shareholders of a company with the sole purpose of making it more difficult for another firm or outsiders to take over a firm against management's wishes. Most poison pills have a trigger point tied to the percentage ownership in the company that is acquired by the potential suitor. Once the trigger point is reached, the other shareholders (the existing shareholders) have the right to buy many additional shares of company stock at low prices. This automatically increases the total number of shares outstanding and reduces the voting power of the firm wishing to acquire the company. A hybrid, or intermediate, security, falling between debt and common stock, is preferred stock. Preferred stockholders are entitled to receive a stipulated dividend and must receive this dividend before any payment is made to common stockholders. Preferred dividends usually accumulate if they are not paid in a given year, though preferred stockholders cannot initiate bankruptcy proceedings or seek legal redress if nonpayment occurs. Finally, common stock, preferred stock, bonds, and other securities tend to receive returns over the long run in accordance with risk, with corporate issues generally paying a higher return than government securities.  *MAIN SOURCE: BLOCK & HIRT, 2005, FOUNDATIONS OF FINANCIAL MANAGEMENT, 11TH ED., PP. 518-522* end |

No comments:

Post a Comment