Process Cost System (Part C)

by

Charles Lamson

|

Bringing It All Together: The Cost of Production Report

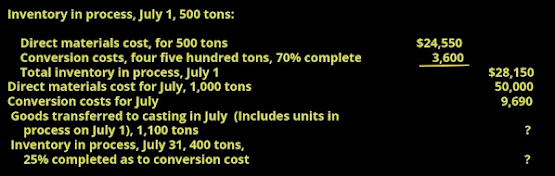

A cost of production report is normally prepared for each processing department at periodic intervals. The July cost of production report for McDermott Steel's Melting Department is shown in Exhibit 7. As can be seen on the report, the two question marks (from part 115 and reintroduced above) can now be determined. The cost of goods transferred to the Casting Department in July was $66,700, while the cost of the ending work in process in the Melting Department on July 31 is $21,140. EXHIBIT 7 Cost of Production Report for McDermott Steel's Melting Department---FIFO %20(2)%20(1)%20(1).jpg) The report summarizes the four previous steps (from part 115) by providing the following production quantity and cost data:

The cost of production report is also used to control costs. Each department manager is responsible for the units entering production and the costs incurred in the department. Any failure to account for all costs and any significant differences in unit product cost from one month to another should be investigated.  Journal Entries for a Process Cost System To illustrate the journal entries to record the cost flows in a process costing system, we will use the July transactions for McDermott Steel. The entries in summary form for those transactions are shown below. In practice, the transactions would be recorded daily. %20(5)%20(1).jpg) Exhibit 8 shows the flow of costs for each transaction. Note that the highlighted amounts in Exhibit 8 were determined from assigning the costs charged to production in the Melting Department. These amounts were computed and are shown at the bottom of the cost of production report for the Melting Department in Exhibit 7. Likewise, the amount transferred out of the Casting Department to Finished Goods would have been determined from a cost of production report for the Casting Department. EXHIBIT 8 McDermott Steel's Cost Flows %20(7)%20(1)%20(2).jpg)  *WARREN, REEVE, & FESS, 2005, ACCOUNTING, 21ST ED., PP. 794-796* end |

No comments:

Post a Comment