Let us begin our discussion of input markets simply by discussing a firm that uses only one variable factor of production.

A Firm Using Only One Variable Factor of Production: Labor

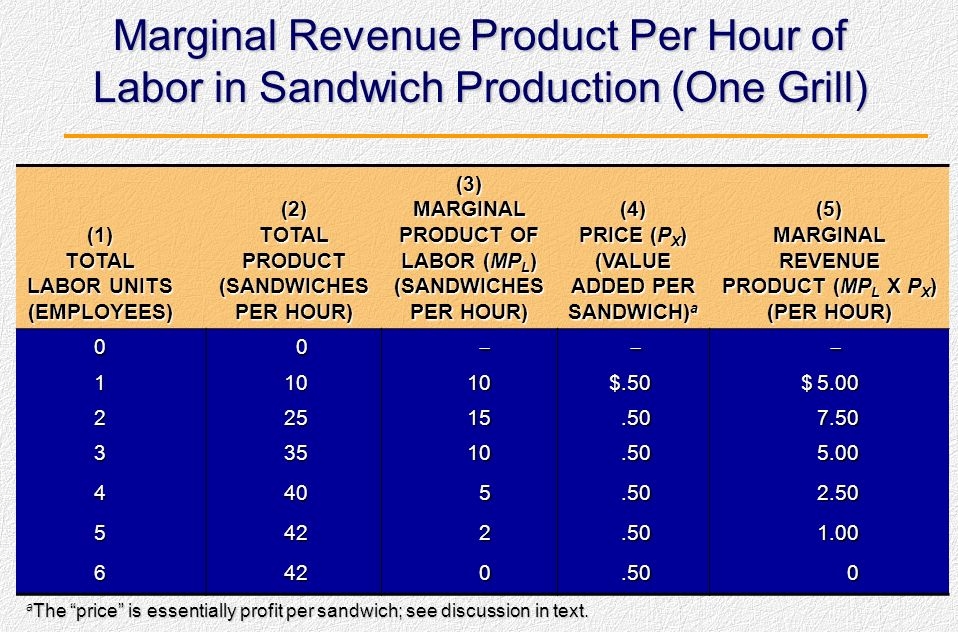

Demand for an input depends on that input's marginal revenue product and its unit cost, or price. The price of labor, for example, is the wage determined in the labor market. (At this point we are continuing the example of the sandwich shop from last post, and we assume that the sandwich shop uses only one variable factor of production---labor. Remember that competitive firms are price takers in both output and input markets. Such firms can hire all the labor they want to hire as long as they pay the market wage.) We can think of the hourly wage at the sandwich shop as the marginal cost of a unit of labor.

A profit-maximizing firm will add inputs in the case of labor, it will hire workers as long as the marginal revenue product of that input exceeds the market price of that input---in the case of labor, the wage.

Look again at the figures for the sandwich shop in Table 1 (from last post and reintroduced below), column five. Now suppose that the going wage for sandwich makers is $4 per hour. A profit-maximizing firm would hire three workers. The first worker would yield $5 per hour in revenues and would yield $7.50, but they each would cost only $4 per hour. The third worker would bring in $5 per hour, but still cost only $4 in marginal wages. The marginal product of the fourth worker, however, would not bring in enough revenue ($2.50) to pay this workers salary. Total profit is thus maximized by hiring three workers.

TABLE 1

Figure 3 presents the same concept graphically. The labor market appears in Figure 3(a); Figure 3(b) shows a single firm that employs workers. This firm, incidentally, does not represent just the firm's single industry. Because firms in many different industries demand labor, the representative firm in figure 3(b) represents any firm in any industry that uses labor.

The firm faces a market wage rate of $10. We can think of this as the marginal cost of a unit of labor. (Note that we are now discussing the margin in units of labor; in previous posts, we talked about marginal units of output.) Given a wage of $10, how much labor would the firm demand?

Thus the curve in Figure 3(b) tells us how much labor a firm that uses only one variable factor of production will hire at each potential market wage rate. If the market wage falls, the quantity of labor demanded will rise. If the market rises, the quantity of labor demanded will fall. This description should sound familiar to you---it is, in fact, the description of a demand curve. Therefore we can now say that when a firm uses only one variable factor of production, that factor's marginal revenue product curve is the firm's demand curve for that factor in the short run.

Comparing Marginal Revenue and Marginal Cost to Maximize Profits In parts 34 through 38 of this analysis, we saw that a competitive firm's marginal cost curve is the same as its supply curve. That is, at any output price, the marginal cost curve determines how much output a profit-maximizing firm will produce. We came to this conclusion by comparing the marginal revenue that a firm would earn by producing one more unit of output with the marginal cost of producing that unit of output.

In both cases, the firm is comparing the cost of production with potential revenues from the sale of product at the margin. In parts 34 through 38 of this analysis, the firm compared the price of output (P, which is equal to MR in perfect competition) directly with cost of production (MC), where cost was derived from information on factor prices and technology. (Review the derivation of cost curves in parts 34 through 38 if this is unclear.) Here, information on output price and technology is contained in the marginal revenue product curve, which is compared with information on input price to determine the optimal level of input to demand.

The assumption of one variable factor of production makes the trade-off facing firms easy to see. Figure 5 shows that in essence firms weigh the value of labor as reflected in the market wage against the value of the product of labor as reflected in the price of output.

Assuming that labor is the only variable input, if society values a good more than it costs firms to hire the workers to produce that good, the good will be produced. In general, the same logic also holds for more than one input. Firms weigh the value of outputs as reflected in output price against the value of inputs as reflected in marginal costs.

Driving Input Demands For the small sandwich shop, calculating the marginal product of a variable input (labor) and marginal revenue product was easy. Although it may be more complex, the decision process is essentially the same for both big corporations and small proprietorships.

When an airline hires more flight attendants, for example, it increases the quality of its service to attract more passengers and sell more of its product. In deciding how many to hire, the airline must figure out how much new revenue the added flight attendants are likely to generate relative to their wages.

At the sandwich shop, diminishing returns set in at a certain point. The same holds true for an airplane. Once a sufficient number of attendants are on a plane, additional attendance adds little to the quality of service, and beyond a certain level might even give rise to negative marginal product. Too many attendants could bother the passengers and make it difficult to get to the restrooms.

In making your own decisions, you, too, compare marginal gains with input costs in the presence of diminishing returns. Suppose you grow vegetables in your yard. First, you save money at the grocery store. Second, you can plant what you like, and the vegetables taste better fresh from the garden. Third, you simply like to work in the garden.

Like the sandwich shop and the airline, you also face diminishing returns. You have only 625 square feet of garden to work with, and with land as a fixed factor in the short run, your marginal product will certainly decline. You can work all day everyday, but your limited space will produce only so many string beans. The first few hours you spend each week watering, fertilizing, and dealing with major weed and bug infestations probably have a high marginal product. However, after five or six hours, there is little else you can do to increase yield. Diminishing returns also apply to your sense of satisfaction. The farmers markets are now full of cheap fresh produce that taste nearly as good as yours. Once you have been out in the garden for a few hours, the hot sun and hard work start to lose their charm.

Although your gardening does not involve a salary (unlike the sandwich shop and the airline, which pay out wages), the labor you supply has a value that must be weighed. When do returns diminish beyond a certain point, you must weigh the value of additional gardening time against leisure and the other options available to you.

Less labor is likely to be employed as the cost of labor rises. If the competitive labor market pushed the daily wage to $6 per hour, the sandwich shop would hire only two workers instead of three (see Table 1).

In the "new economy" there is a common example of what may seem to be an exception to the rule that workers will only be hired if the revenues they generate are equal to or greater than their wages. Many startup companies pay salaries to workers before they begin to take in revenue. How does a company pay workers if it is not earning any revenues? The answer is that the entrepreneur, or the venture capital fund supporting the entrepreneur, is betting that the firm will earn substantial revenues in the future. Workers are hired because the entrepreneur expects that their current efforts will produce future revenues greater than their wage costs.

*CASE & FAIR, 2004, PRINCIPLES OF ECONOMICS, 7TH ED., PP. 201-205*

|