Input Demand: The Labor and Land Markets

(Part A)

by

Charles Lamson

|

All business firms must make three decisions: (1) how much to produce and supply in output markets; (2) how to produce that output---that is, which technology to use; and (3) how much of each input to demand. So far, our discussion of firm behavior has focused on the first two questions. In parts 30 through 44 of this analysis, it is explained how profit-maximizing firms choose among alternative technologies and decide how much to supply in output markets.

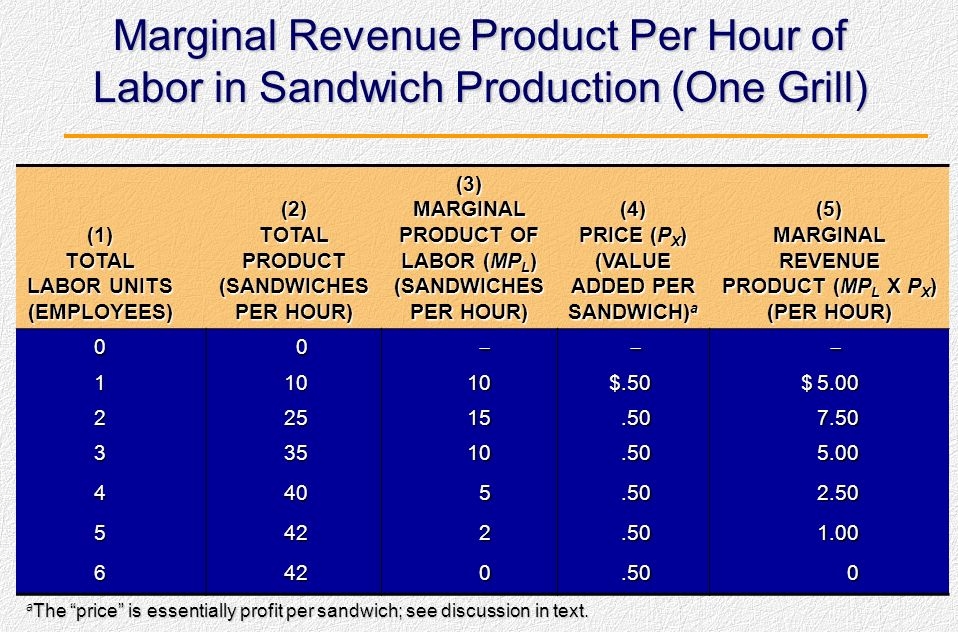

We now turn to the behavior of firms in perfectly competitive input markets, going behind input demand curves in much the same way that we went behind output supply curves in the previous posts mentioned above. When we look behind input demand curves, we discover the exact same set of decisions that we saw when we analyzed output supply curves. In a very real sense, we have already talked about everything covered in the next few posts. It is the perspective that is new. The three main inputs are labor, land, and capital. Transactions in the labor and land markets are fairly straightforward. Households supply their labor to firms that demanded it in exchange for a salary or wage. Landowners sell or rent land to others. Capital markets are a bit more complex but are conceptually very similar. Households supply the resources used for the production of capital by saving and giving up present consumption. Savings flow through financial markets to firms that use these savings to procure capital to be used in production. Households receive interest, dividends, or profits in exchange. The next few posts discuss input markets in general, while focusing on the capital market in some detail. Figure 1 outlines the interactions of households and firms in the labor and capital markets.  Input Markets: Basic Concepts Before we begin our discussion of input markets, it will be helpful to establish some basic concepts: derived demand, complementary and substitutable inputs, diminishing returns, and marginal revenue product.  Demand for Inputs: A Derived Demand A firm cannot make a profit unless there is a demand for its product. Households must be willing to pay for the firm's output. The quantity of output that a firm produces (in both the long and the short run) thus depends on the value placed by the market on the firm's product. This means that demand for inputs depends on the demand for outputs. In other words, input demand is derived from output demand. The value attached to a product and the input needed to produce that product define the input's productivity. Normally, the productivity of an input is the amount of output produced per unit of that input. When a large amount of output is produced per unit of an input, the input is said to be highly productive. When only a small amount of output is produced per unit of the input, the input is said to exhibit low productivity. Inputs are demanded by a firm if and only if households demand the good or service produced by that firm. Prices in competitive input markets depend on firms' demand for inputs, households' supply of inputs, and interaction between the two. In the labor market, for example, households must decide whether to work and how much to work. The opportunity cost of working for a wage is either the leisure or the value derived from unpaid labor---working in the garden, for instance, or raising children. In general, firms will demand workers as long as the value of what those workers produce exceeds what they must be paid. Households will supply labor as long as the wage they receive exceeds the value of leisure or the value that they derive from nonpaid work.  Inputs: Complementary and Substitutable Inputs can be complementary or substitutable. Two inputs used together may enhance, or compliment, each other. For example, a new machine is useless without someone to run it. Machines can also be substituted for labor, or less often perhaps labor can be substituted for machines. All this means that a firm's input commands are highly linked to one another. An increase or decrease in wages naturally causes the demand for labor to change, but it may also have an effect on the demand for capital or land. If we are to understand the demand for inputs, therefore, we must understand the connections among labor, capital, and land. Diminishing Returns If you have been following along, you will recall that the short run is the period during which some fixed factor of production limits a firm's capacity to expand. Under these conditions, the firm that decides to increase output will eventually encounter diminishing returns. Stated more formally, a fixed scale of plant means that the marginal product of variable inputs eventually declines.   In parts 30 through 33 of this analysis, we talked at some length about declining marginal product at a sandwich shop. The first two columns of Table 1 reproduce some of the production data from that shop. You may remember that the shop has only one grill, at which only two or three people can work comfortably. In this example, the grill is the fixed factor of production in the short run. Labor is the variable factor. The first worker can produce 10 sandwiches per hour, and the second can produce 15 (see column 3 of Table 1). The second worker can produce more because the first is busy answering the phone and taking care of customers, as well as making sandwiches. After the second worker, however, marginal product declines. The third worker adds only 10 sandwiches per hour, because the grill gets crowded. The fourth worker can squeeze in quickly while the others are serving or wrapping, but adds only five additional sandwiches each hour, and so forth. TABLE 1  In this case, the grill's capacity ultimately limits output. To see how the firm might make a rational choice about how many workers to hire, we need to know more about the value of the firm's product and the cost of labor. Marginal Revenue Product The marginal revenue product (MRP) of a variable input is the additional revenue a firm earns by employing one additional unit of that input, ceteris paribus. If labor is the variable factor, for example, hiring an additional unit will lead to added output (the marginal product of labor). The sale of that added output will yield revenue. Marginal revenue product is the revenue produced by selling the good or service that is produced by the marginal unit of labor. In a competitive firm, marginal revenue product is the value of a factor's marginal product.    *CASE & FAIR, 2004, PRINCIPLES OF ECONOMICS, PP. 197-201* end |

No comments:

Post a Comment