Rather than dividing the world between good and evil, the Left divided the world in terms of economics. Economic classes, not moral values, explained human behavior. Therefore, to cite a common example, poverty, not one's moral value system, or lack of it, caused crime.

Demand and Supply Applications and Elasticity

(Part A)

by

Charles Lamson

|

Every society has a system of institutions that determines what is produced, how it is produced, and who gets what is produced. In some societies, these decisions are made centrally, through planning agencies or by government directive. However, in every society many decisions are made in a decentralized way, through the operation of markets.

Markets exist in all societies, and Parts 9 through 15 of this analysis provided a bare-bones description of how markets operate. In the next several posts, we continue our examination of demand, supply, and the price system. The Price System: Rationing and Allocating Resources The market system, also called the price system, performs two important and closely related functions. First, it provides an automatic mechanism for distributing scarce goods and services. That is, it serves as a price rationing device for allocating goods and services to consumers when the quantity demanded exceeds the quantity supplied. Second, the price system ultimately determines both the allocation of resources among producers and the final mix of outputs.

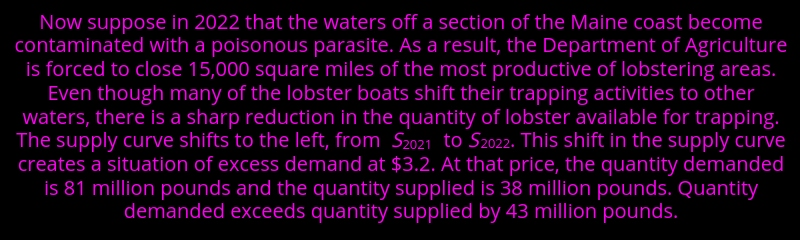

Price Rationing Consider first the simple process by which the price system eliminates a shortage. Figure 1 shows hypothetical supply and demand curves for lobsters caught off the coast of New England.  Lobsters are considered a delicacy. Maine produces most of the lobster catch in the United States, and anyone else who drives up the Maine coast cannot avoid the hundreds of restaurants selling lobster rolls, steamed lobster, and baked stuffed lobster. As Figure 1 shows, the equilibrium price of live New England lobsters is $3.27 per pound in 2021. At this price, lobster boats bring in lobsters at a rate of 81 million pounds per year---an amount that is just enough to satisfy demand. Market equilibrium exists it at $3.27 per pound, because at that price quantity demanded is equal to quantity supplied. (Remember from last post that equilibrium occurs at the point where the supply and demand curves intersect. In Figure 1 this occurs at Point C.)  The reduced supply causes the price of lobster to rise sharply. As the price rises, the available supply is rationed. Those who are willing and able to pay the most get it. You can see the market's price rationing function clearly in Figure 1. As the price rises from $3.27, the quantity demanded declines along the demand curve, moving from point C (81 million pounds) toward point B (60 million pounds). The higher prices mean that restaurants must charge much more for lobster rolls and stuffed lobsters. As a result, many people simply stop buying lobster or order it less frequently when they dine out. Some restaurants drop it from the menu entirely, and some shoppers at the fish counter turn to lobster substitutes such as swordfish and salmon.  As the price rises, lobster trappers (suppliers) also change their behavior. They stay out longer and put out more traps than they did when the price was $3.27 per pound. Quantity supplied increases from 38 million pounds to 60 million pounds. This increase in price brings about a movement along the 2022 supply curve from point A to point B. Finally, a new equilibrium is established at a price of $4.50 per pound and a total output of 60 million pounds. The market has determined who gets the lobsters: The lower total supply is rationed to those who are willing and able to pay the higher price. This idea of "willingness to pay" is central to the distribution of available supply, and willingness depends on both desire (preferences) and income/wealth. Willingness to pay does not necessarily mean that only the very rich will continue to buy lobsters when the price increases. Lower-income people may continue to buy some lobster, but they will have to be willing to sacrifice more of other goods to do so. In sum:  There is some price that will clear any market you can think of. Consider the market for a famous painting such as Van Gogh's Portrait of Dr. Gachet, Illustrated in Figure 2. At a low price, there would be an enormous demand for such an important painting. The price would be bid up until there was only one remaining demander. Presumably, that price would be very high. In fact, Van Gogh's Portrait of Dr. Gachet sold for a record $82.5 million in 1990. If the product is in strictly scarce supply, as a single painting is, its price is said to be demand determined. That is, it is determined solely and exclusively by the amount that the highest bidder or highest bidders are willing to pay.  One might interpret the statement that "there is some price that will clear any market" to mean "everything has its price," but that is not exactly what it means. Suppose you own a small silver bracelet that has been in your family for generations. It is quite possible that you would not sell it for any amount of money. Does this mean that the market is not working, or that quantity supplied and quantity demanded are not equal? Not at all. It means simply that you are the highest bidder. By turning down all bids, you must be willing to forgo what anybody offers for it.  *MAIN SOURCE: CASE & FAIR, 2004, PRINCIPLES OF ECONOMICS, 7TH ED., PP. 71-73* end |

No comments:

Post a Comment